A3 Depreciation

Depreciation is the reduction in value of assets over time. This can be due to wear and tear or the asset becoming obsolete. You may find depreciation on the statement of financial position as it reduces the value of non-current assets and you may also find it on the statement of comprehensive income as a cost. Two methods of calculating depreciation are the straight-line method and the reducing balance method.

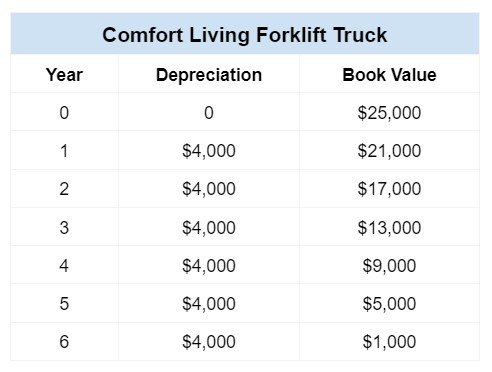

The Straight Line Method

To calculate the annual depreciation, the following formula is used

Annual depreciation = (purchase cost - salvage value) / lifespan

Example

At the start of operations, Comfort Living bought a forklift truck for $25,000 and its expected to last 6 years. Its salvage value is expected to be $1,000.

Annual depreciation = $25,000 - $1,000 / 6 = $4,000

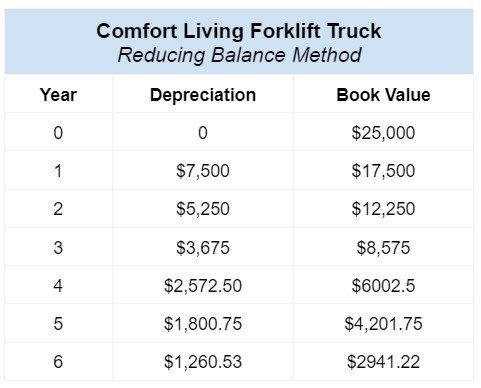

The Reducing Balance Method

The reducing balance method depreciates the value of the asset by a percentage of the previous years net book value. The formula used is

Net book value = Last year’s net book value - percentage depreciation

Example

Comfort Living expect their forklift truck to depreciate by 30% each year.