B2 Completion of Cash Flow Statements

Cash flow statements must be completed according to the format in IAS7. Cash flows should therefore be classified as;

Operating activities

Investing activities

Financing activities

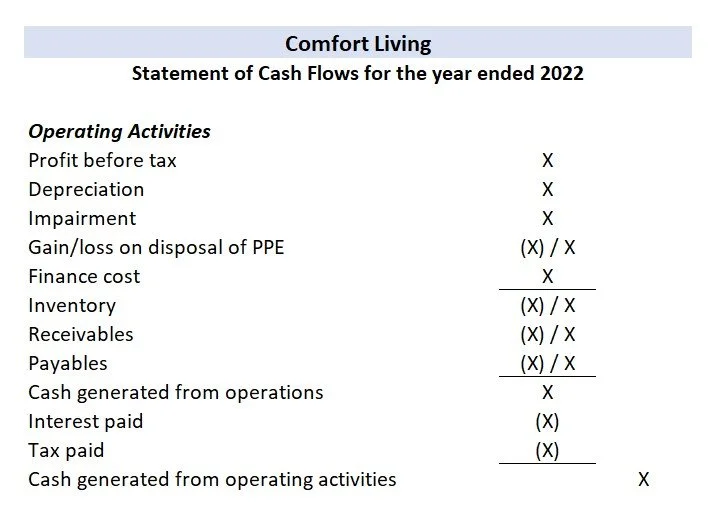

Cash Flow from Operating Activities

This is the first section of the statement of cash flows. This section details the flow of money generated from the business’ main activity. This is generally the manufacture and sale of goods or the provision of services. This section allows stakeholders to analyse the sucess of the core functions of the business.

The indirect method takes the net profit figure from the profit and loss account and applies adjustments

Cash Flow from Investing Activities

This is the section on the cash flow statement that lists the inflows and outflows related to investment activities. This includes spending on assets and securities such as stocks and bonds or the sale of assets and securities.

Property, Plant and Equipment (PPE) refers to spending on non-current assets which are invested in as they are expected to return economic benefits to the company.

Cash Flow from Financing Activities

This section of the cash flow statement itemises the cash inflows and outflows related to generating funding for the company. This includes sales of shares, borrowing and dividends received.